🔑 AML vs KYC: what's the difference in crypto compliance

The crypto market in the United States has grown past $2 trillion in total capitalization, and with that growth, stricter rules from federal regulators have emerged. Two terms dominate every compliance conversation in crypto regulation. Most people treat them as the same thing, but the AML vs KYC distinction is real and meaningful. One covers the full scope of anti-money laundering monitoring, while the other focuses on verifying a user's identity before granting access to financial services.

🔍 Understanding AML and KYC in crypto compliance

Both systems exist to protect financial platforms and their users from fraud, theft, and illegal activity. In crypto, these systems have become mandatory for any exchange or wallet provider operating in the US market. When people compare AML vs KYC, they often assume both terms describe the same process. The way each one works is fundamentally different.

🛡️ What AML means in financial monitoring

Anti-Money Laundering refers to the set of rules, processes, and technologies that financial institutions use to detect and prevent illicit fund flows. In crypto, transaction monitoring AML runs 24/7 across all user accounts. The system flags unusual patterns, sudden volume spikes, transfers to high-risk jurisdictions, or rapid fund movements between wallets.

This is not a one-time check. While KYC and AML serve separate roles, transaction data flows continuously into automated AML monitoring systems that score activity based on risk models. When something looks suspicious, the platform files a Suspicious Activity Report (SAR) with FinCEN.

- 🔹 Tracks cross-border fund movements in real time

- 🔹 Flags structuring attempts (breaking large sums into smaller deposits)

- 🔹 Identifies connections to sanctioned wallets or entities

- 🔹 Generates automated risk scores for every transaction

✅ What KYC means for user verification

Know Your Customer is the second pillar of crypto compliance. It is the process of confirming a user's real identity before they can trade, deposit, or withdraw funds. In crypto, identity verification crypto typically happens during account registration. Users submit government-issued ID, proof of address, and sometimes a selfie for biometric matching.

Without proper KYC meaning crypto platforms cannot assess individual user risk. The KYC onboarding process usually takes between 5 minutes and 48 hours depending on the platform.

| Feature | 🛡️ AML | ✅ KYC |

|---|---|---|

| Full name | Anti-Money Laundering | Know Your Customer |

| Primary goal | Detect and prevent illicit fund flows | Verify user identity |

| When it runs | Continuously, post-registration | During onboarding + periodic reviews |

| Data used | Transaction patterns, wallet addresses | Government ID, proof of address, biometrics |

| Regulatory body (US) | FinCEN, DOJ | FinCEN, SEC, state regulators |

🔗 Why both systems are used together

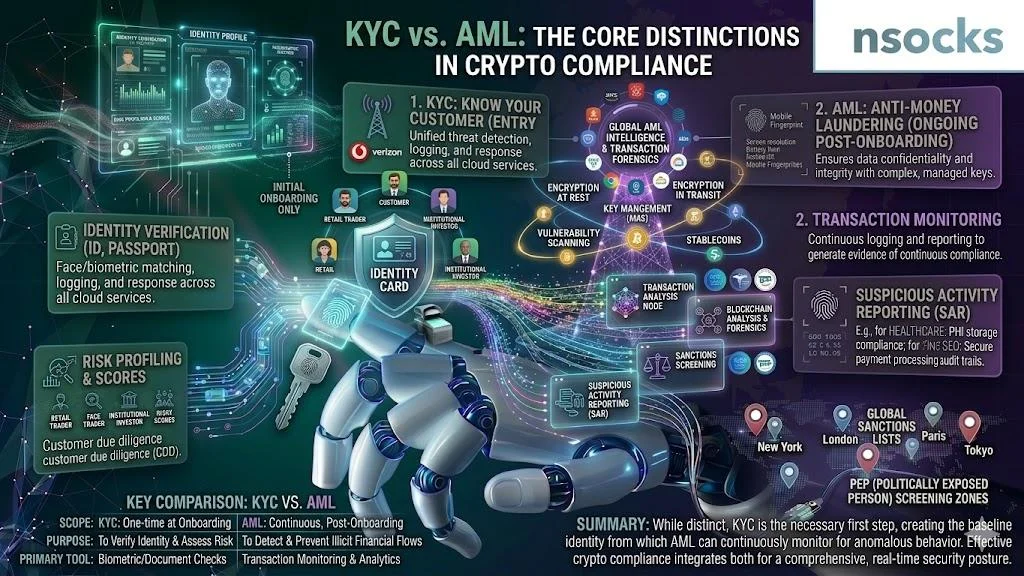

Running identity verification without transaction monitoring is like checking IDs at the door but ignoring what happens inside. Combining these two systems creates a layered defense that regulators call a compliance workflow crypto framework. Each layer catches what the other misses. A verified identity means nothing if the person later launders money through the platform. Together, these systems form the backbone of any serious AML KYC compliance program.

⚖️ Key differences between AML and kyc systems

The difference between AML and KYC becomes clearer when you look at what each system does on a daily basis. They serve different purposes, collect different data, and activate at different stages of the user experience.

🎯 Focus and purpose differences

One system is about identity. The platform needs to know who this person is, where they live, and whether they are legally allowed to use financial services. The other is about behavior, tracking whether a person engages in suspicious activity with their money.

The first asks "Who are you?" while the second asks "What are you doing?" One is a snapshot taken at registration. The other is a continuous movie playing for as long as the account exists. This fundamental split is the main reason people confuse these two terms, and why understanding KYC vs AML matters for platform operators.

📂 Data collection and usage

KYC data collection happens upfront. A user uploads their passport or driver's license. The platform verifies the document against databases, checks for sanctions matches, and assigns an initial risk score. Transaction data accumulates over time; every deposit, withdrawal, trade, and transfer gets logged and analyzed against historical patterns.

This split in data handling is one of the clearest AML vs KYC distinctions. Both datasets feed into a platform's overall risk management frameworks but serve separate analytical purposes.

| Criteria | 🛡️ AML System | ✅ KYC System |

|---|---|---|

| Data type | Transaction logs, wallet analytics | Personal documents, biometric data |

| Collection method | Automated monitoring tools | User submission + third-party verification |

| Update frequency | Real-time / continuous | At onboarding + periodic re-verification |

| Risk assessment | Transaction-based risk scoring | Identity-based risk profiling |

| Reporting output | SARs filed with FinCEN | Verified user profiles stored internally |

| US legal basis | Bank Secrecy Act (BSA) | USA PATRIOT Act, BSA |

⏱️ Timing in user journey

Identity checks happen at the gate. Transaction monitoring kicks in after entry. This timing gap is one of the most practical AML vs KYC differences to keep in mind. A standard user identity validation flow follows a predictable sequence.

- 📝 User registers with email and password

- 🪪 Platform requests government-issued ID and proof of address

- 🤳 User completes biometric verification (selfie or video)

- ⏳Verification team reviews and approves (5 min to 48 hours)

- ✅ Account activated, user can deposit and trade

- 🔍 Automated monitoring begins on the first transaction

- 🚩 Alerts generated if behavior crosses risk thresholds

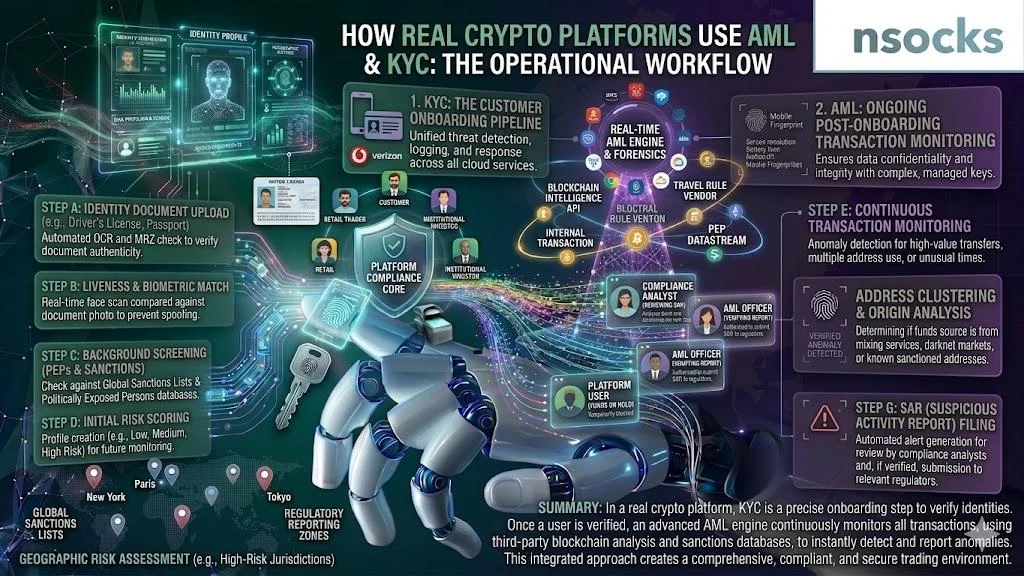

💻 How AML and kyc work in real crypto platforms

US-based crypto exchanges handle millions of users and billions in daily volume. The KYC AML process must scale without creating bottlenecks or exposing the platform to regulatory risk. Effective crypto compliance systems automate as much as possible while keeping human oversight for edge cases.

👤 User onboarding process

Most US crypto exchanges use a tiered onboarding model. Full access demands complete identity verification through a customer due diligence process, and this is where the AML vs KYC workflow splits into separate tracks. Users provide their full legal name, date of birth, Social Security Number, and a photo of their government ID.

- 🖥️ User selects verification tier (Basic / Intermediate / Advanced)

- 📄 System requests documents matching the selected tier

- 🤖 Automated OCR scans the document for data extraction

- 🔎 Third-party service cross-references data against government databases

- ✅ Verification status updated, user gains corresponding access level

🔎 Transaction monitoring after verification

After verification, every trade, deposit, and withdrawal is added to the monitoring pipeline. This post-verification stage is where the AML vs KYC handoff becomes most visible. Platforms use compliance verification methods combining rule-based triggers with machine learning models. A user who normally trades $500 per week but suddenly moves $50,000 in a single day will trigger an alert.

- 🔹 User behavior changes over time, and risk profiles must adapt

- 🔹 New sanctions lists get published regularly, and existing users must be re-screened

- 🔹 Account takeover fraud can turn a legitimate account into a laundering tool

🔄 Continuous compliance systems

Modern crypto platforms run compliance 24/7. Some re-verify user identities every 12 months. Others trigger re-verification based on risk events. The KYC AML policy at most US exchanges mandates both scheduled and event-driven reviews.

| Process | Frequency | Action |

|---|---|---|

| 🔍 Transaction screening | Real-time | Automated risk scoring |

| 🪪 Identity re-verification | Every 12-24 months | Document re-submission |

| 🌍 Sanctions screening | Daily | Cross-reference all users |

| 🚩 SAR filing | As needed | Report to FinCEN within 30 days |

🏛️ Regulatory framework in the united states

US crypto regulation is not governed by a single agency. Multiple federal and state bodies share oversight, making AML KYC regulations among the most complex globally.

🏢 Role of financial regulators

FinCEN sits at the center of US anti-money laundering enforcement. All Money Services Businesses, including crypto exchanges, must register, run anti-money laundering programs, and file SARs. The SEC oversees crypto assets classified as securities. State-level regulators like New York's BitLicense add another layer, making the AML vs KYC obligations even more complex. The financial regulation crypto landscape in the US is arguably the most demanding worldwide.

📋 Compliance requirements for crypto companies

Every crypto company operating in the US must meet a baseline set of obligations. Failure results in fines, license revocation, or criminal prosecution.

| Requirement | Responsible agency | Penalty for non-compliance |

|---|---|---|

| 🏦 MSB Registration | FinCEN | Up to $250,000 per violation |

| 🛡️ AML Program | FinCEN | Civil and criminal penalties |

| ✅ KYC Verification | FinCEN | Enforcement action, license loss |

| 📄 SAR Filing | FinCEN | $100,000+ per missed report |

| 📊 CTR Filing (>$10,000) | FinCEN | Up to $250,000 fine |

🌐 Impact on users and businesses

Regulation creates friction: longer onboarding, stricter withdrawal limits, and more document requests. But it also creates trust. Institutional investors will not touch platforms lacking proper compliance. The compliance framework, when implemented correctly, opens doors that would otherwise remain shut. Banks refuse services to companies that skip KYC and AML checks.

✅ Benefits of AML and kyc for crypto ecosystem

Both systems generate real benefits for platforms and users alike. Understanding AML vs KYC is not just an academic exercise. It directly affects how well a platform protects its community. The path toward mainstream crypto acceptance runs through effective compliance.

🛡️ Fraud prevention and risk reduction

Fraud costs the US financial system billions annually. Properly configured KYC and AML systems reduce exposure on both sides. Platforms catch bad actors earlier. Users lose money less often.

✅ Benefits

- 🟢 Reduced account takeover through biometric verification

- 🟢 Faster detection of structuring and layering attempts

- 🟢 Lower chargeback rates on fiat on-ramps

- 🟢 Reduced exposure to sanctioned entities

❌ Limitations

- 🔴 No system catches 100% of illicit activity

- 🔴 False positives create friction for legitimate users

- 🔴 Compliance costs get passed to users through fees

🤝 Increased trust and transparency

When users know a platform verifies identities and monitors transactions, they feel safer depositing larger amounts. The AML vs KYC distinction may seem abstract, but the combined effect builds real confidence. Transparency reports show how many SARs were filed and what percentage of transactions were flagged. More trust brings more users, more liquidity, and more institutional capital.

🏦 Institutional adoption of crypto

Banks, hedge funds, and asset managers will not invest in platforms lacking equivalent safeguards. Robust crypto KYC programs are a requirement for institutional participation.

A mid-sized US hedge fund reviewing five exchanges in 2024 rejected three immediately for weak SAR filing, no continuous monitoring, and poor customer due diligence. Only platforms with proven KYC AML crypto infrastructure passed. Total compliance review: 14 weeks.

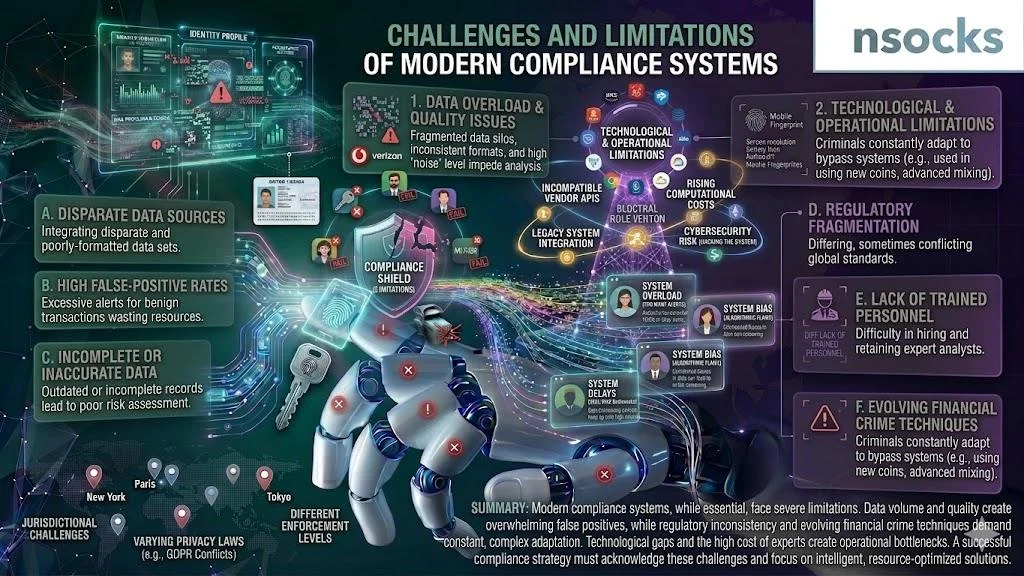

⚠️ Challenges and limitations of compliance systems

No compliance system is flawless. Even with a clear AML vs KYC structure in place, both systems create real operational challenges for platforms and their users. Cost, friction, and privacy risks are the three biggest pain points that every US crypto company must manage daily.

😤 User experience friction

The average US crypto user must provide 4-7 documents during onboarding. Verification takes 5 minutes to 72 hours. Despite clear AML vs KYC benefits, a 2024 survey found roughly 25% of users never complete verification due to excessive document requests and long wait times.

🔒 Data privacy concerns

Mandatory identity verification conflicts with crypto's original privacy ethos. Users hand over passports, Social Security Numbers, and home addresses. While KYC and AML protect against fraud, they also create honeypots of sensitive data. Data breaches at crypto companies have exposed millions of records. This tension between compliance and privacy remains one of the most debated industry topics.

💰 Operational costs for companies

A mid-tier US crypto exchange spends between $2 million and $10 million annually on compliance. When weighing AML vs KYC costs separately, transaction monitoring typically eats the bigger budget. That includes monitoring software, compliance officer salaries, legal fees, and audit costs.

- 🔹 Automating document verification reduces manual review by 60-80%

- 🔹 Risk-based tiering means low-risk users get cheaper processing

- 🔹 Cloud-based monitoring tools scale with transaction volume

- 🔹 Shared verification utilities accept checks from other licensed providers

📊 Comparison table: AML vs KYC at a glance

This puts the full picture side by side across every major dimension. When comparing these two systems at scale, the distinctions are sharp, they serve different functions within a shared compliance objective. This table covers the most frequently asked AML vs KYC questions in one place.

| Dimension | 🛡️ AML | ✅ KYC |

|---|---|---|

| Purpose | Prevent money laundering and terrorist financing | Verify user identity and assess individual risk |

| Timing | Continuous, starts after first transaction | Primarily at onboarding, with periodic re-checks |

| Data type | Transaction records, wallet analytics | Government IDs, proof of address, biometrics |

| Function | Monitor, detect, report suspicious activity | Identify, verify, classify users by risk level |

| User impact | Mostly invisible unless alert triggered | Direct interaction required (document upload) |

🌍 Real-world use cases in crypto industry

A US-based exchange processing 15,000 registrations daily auto-approves 82% within 3 minutes. The remaining 18% go to manual review (average 6 hours). This is where AML vs KYC roles become clearly visible in daily operations. Once approved, every first transaction triggers monitoring activation. Within 30 days, roughly 0.4% of new accounts generate an alert. About 15% of those result in SAR filing.

| Use case | KYC role | AML role |

|---|---|---|

| 🆕 New user signup | Verify identity, assign risk tier | Not active yet |

| 💸 Large withdrawal ($25,000+) | Confirm identity matches holder | Flag if pattern is unusual |

| 🌐 Cross-border transfer | Check nationality and sanctions | Monitor destination wallet |

| 🔄 Recurring small deposits | Already verified | Detect structuring patterns |

| 🏦 Fiat off-ramp to bank | Re-verify if dormant > 12 months | Check for layering |

🔮 Future of AML and KYC systems

Zero-knowledge proofs could let users verify identity without exposing personal documents. On-chain analytics tools trace funds across privacy-focused blockchains with growing accuracy. AI-driven monitoring reduces false positive rates. Some platforms report 40% improvement after switching to ML-based systems. The relationship between these two systems will likely tighten as technology matures.

FinCEN proposed rules in 2024 extending reporting requirements to DeFi protocols. The SEC continues pushing for clearer definitions of which crypto assets qualify as securities. Platforms building strong compliance frameworks now will be better positioned as rules take effect. The KYC and AML landscape is shifting toward decentralized identity solutions. Self-sovereign identity (SSI) wallets could store verified credentials presented across multiple platforms, reducing redundant verification without sacrificing compliance.

❓ Frequently asked questions

What is the main difference between AML and KYC?

One system tracks transactions, the other confirms user identity.

Is KYC part of AML compliance?

Yes, it is one component of a broader anti-money laundering program.

Why do crypto exchanges require KYC?

US law requires identity checks for all Money Services Businesses.

Can AML work without KYC?

It can flag activity, but enforcement needs a verified identity behind the account.

Is KYC mandatory in the united states?

Yes, for all regulated financial platforms.